How we picked the best crypto cards

Choosing a crypto debit card requires looking past the marketing hype to the actual cost of spending. We evaluated the top contenders based on four strict criteria: fee structures, cashback rates, supported cryptocurrencies, and regional availability. Our goal was to identify cards that function as reliable daily spending tools rather than speculative assets.

Fee structures are the most critical factor. Many cards advertise zero monthly fees but charge steep foreign transaction fees or high conversion spreads when you spend outside your home currency. We prioritized cards with transparent fee schedules and low conversion rates to avoid hidden costs that erode your balance over time.

Cashback rates and supported cryptocurrencies determine the card's utility. We compared real cashback percentages after fees for major coins like Bitcoin and Ethereum. Cards that support a wide range of stablecoins or allow you to choose which asset to spend at the point of sale offer significantly more flexibility for everyday purchases.

Regional availability remains a major constraint. While many cards are marketed globally, they often restrict users in specific countries due to regulatory requirements. We verified the current availability of each card to ensure you can actually apply and use it. For a detailed breakdown of how to weigh these factors, refer to the Bitcoin Foundation's 2026 guide on choosing a crypto debit card.

Best overall crypto debit card

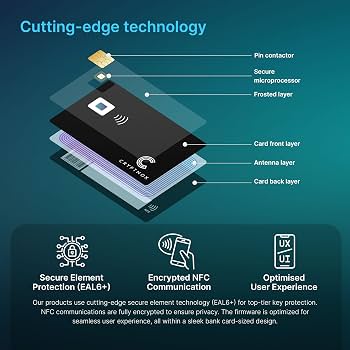

The Crypto.com Visa Card stands out as the best overall crypto debit card for most users in 2026. It offers the most transparent rewards structure, allowing you to earn cashback in either USDT or the native CRO token. This flexibility is critical: you can choose stablecoin rewards to avoid volatility or stake CRO to boost your percentage. The card’s tiered system is straightforward—higher monthly spend or larger CRO stakes provide better rates, ranging from 1% to 5% cashback.

Beyond rewards, the card integrates seamlessly with the Crypto.com app, giving you instant access to your balance and spending history. You can freeze or unfreeze the card instantly if you suspect fraud, a standard but essential security feature for any financial tool. The metal build quality varies by tier, but even the entry-level plastic card is fully functional for online and contactless payments worldwide.

One minor drawback is the requirement to stake CRO for the higher-tier benefits. If you are not already invested in the Cronos ecosystem, this adds a layer of complexity and market risk. However, for those willing to hold the token, the effective cashback rates often exceed traditional fiat rewards cards. The card is widely accepted, making it a practical daily driver for crypto natives.

As an Amazon Associate, we may earn from qualifying purchases.

Best cards for high cashback rewards

If you spend crypto daily, standard fee structures don't matter as much as the return you get on every transaction. The best crypto debit cards for high cashback rewards function like a high-yield savings account that spends automatically. These cards typically require you to lock up tokens or maintain a specific balance in their native ecosystem to achieve the highest percentage returns.

For example, holding a stablecoin or a volatile asset in a custodial wallet often triggers tiered rewards. You might earn 1% on basic spending, but jump to 4% or more by staking the card's proprietary token. This model benefits users who are already bullish on the ecosystem and willing to lock capital for months.

Below is a comparison of the top performers currently offering the highest net cashback after fees. These cards prioritize reward density over broad acceptance, making them ideal for secondary spending or users who can manage the token volatility.

These rewards are rarely flat. They are dynamic and tied to your portfolio composition. If you hold a diversified basket of assets, you may find that a card like Nexo offers a simpler, albeit lower, 1% return without complex tier management. Conversely, if you are willing to concentrate your holdings in a single ecosystem like Crypto.com or Coinbase, the rewards can significantly offset daily transaction costs.

When choosing a high-reward card, calculate the annual percentage yield (APY) of the required staking against the cashback value. If the token price drops while you are staking, your effective cashback rate may turn negative. Always check the unstaking period to ensure your liquidity needs align with the lock-up requirements.

Best options for low fees and EU users

Regional constraints often define the practical value of a crypto debit card. Users in the European Union face specific regulatory requirements, while fee-sensitive spenders need clarity on foreign transaction costs. This section highlights cards that prioritize low fees and EU compliance, ensuring your spending doesn't erode your returns.

Coinbase Card

The Coinbase Card remains a strong entry point for EU residents due to its straightforward fee structure and regulatory compliance within the European Economic Area (EEA). It allows you to spend crypto directly from your Coinbase account, converting assets at the point of sale. For users focused on low fees, the card typically charges no monthly fees and offers 0% foreign transaction fees on purchases, a significant advantage for travelers or those buying from international merchants. Rewards are paid in the crypto you hold, helping to offset any potential network costs.

Crypto.com Visa Card

Crypto.com offers a tiered Visa card system that appeals to users looking to minimize fees through higher commitment levels. While the basic tier is accessible, higher tiers (such as the Metal or Icy Blue cards) waive foreign transaction fees entirely and offer increased cashback rewards. For EU users, Crypto.com has established compliance with local financial regulations, making it a viable option for daily spending. The key consideration is that maximizing the "low fee" benefit often requires locking up a significant amount of their native CRO token, which may not suit everyone's liquidity preferences.

Kast Card

Kast (formerly known as Kast.io) has emerged as a specialized option for users seeking minimal friction and low fees. It focuses on providing a seamless experience with competitive foreign transaction fees and no annual fees for its standard tiers. For EU users, Kast's approach to compliance and integration with local payment networks makes it a practical choice for those who want to avoid the complexity of traditional banking rails. Its design prioritizes the user's spending power by reducing the overhead costs associated with cross-border transactions.

Crypto card fees to watch for

Crypto debit cards promise to turn digital assets into everyday spending power, but the cost of that convenience often hides in the fine print. Before you link your wallet to a card, it helps to understand where the money actually goes. Many providers advertise low or zero annual fees but charge steep rates on FX conversions and ATM withdrawals.

Foreign exchange (FX) fees

When you spend crypto in a currency different from your card’s base currency, an FX fee applies. This is often the most significant hidden cost. Standard banks typically charge around 3% for international transactions. Crypto cards vary widely; some charge 1% or 2%, while others may charge higher rates during peak times.

Look for cards that offer multi-currency wallets or real-time conversion at interbank rates. For example, the Gnosis Pay card is known for competitive FX structures compared to legacy providers. Always check the specific percentage listed in the cardholder agreement rather than relying on marketing materials that say "low fees."

ATM withdrawal fees

Using your crypto card at an ATM triggers two potential charges. First, the card provider may impose a flat fee per withdrawal, ranging from $2 to $5. Second, the ATM operator itself may charge an access fee. These costs stack quickly, especially if you are withdrawing small amounts frequently.

Some cards, like those from Crypto.com, offer free ATM withdrawals up to a certain monthly limit (e.g., $100 or $500 depending on your tier). Beyond that limit, fees apply. If you rely on cash for daily expenses, choose a card with a generous free withdrawal tier or use your card for point-of-sale purchases instead.

Inactivity and other hidden costs

Beyond FX and ATM fees, watch for inactivity fees. Some providers charge a monthly or annual fee if you do not use the card for a set period, such as six months. This is designed to encourage active usage. Additionally, some cards charge for instant transfers or balance checks.

Review the full fee schedule before applying. Focus on the specific products that match your spending habits. If you travel often, prioritize low FX fees. If you use cash, prioritize low ATM fees. Understanding these costs helps you avoid unexpected deductions from your crypto balance.

No comments yet. Be the first to share your thoughts!